Let’s start today’s LIFEies with this crazy stat: 48% of ALL American households headed by someone over 55 years of age have NO retirement savings whatsoever.

Now, let’s look at the average retirement savings by age:

I strongly believe, we can do better. How?

–Lower your lifestyle and delay gratification We lived in the house I owned before we got married and had 4 kids before we moved to a bigger home. Then…see the last bullet below.

–Pay yourself first. Take money from every paycheck and put it toward investing. Start now. I have been a compulsive investor since I made my first commission and remain so today.

–When you make more money, don’t increase your lifestyle. I have lived in two houses since I started my career 38 years ago. I have owned 3 cars in 28 years.

–If you have debt, follow the “debt snowball method” from Dave Ramsey.

–Increase your financial education. Yes, Robert and Kim Kiyosaki are friends. Yes, they follow what they write. Yes, read this book.

I hope all of my LIFEies readers are saving, getting ahead, investing in and living a Fantastic life. If you are not, you can change, and you can change now. Read below for more on this topic.

![]()

Rule # 2: Be Crystal Clear on What You Want

What kind of retirement do you want? Have you ever sat down and seriously mapped it out? Until you know exactly what you want, you won’t make any progress towards that end goal.

Average Retirement Savings by Age, How you Compare, and What to Do About it

An average retirement may not be your cup of tea, so here’s how to step up your game.

![]()

By: Brian Feutz | Published on December 2, 2021

Another one: The average Social Security benefit this year is $1,543.

Do the math. If you have no savings and you’re an average earner, you’ll be living on $1,543 a month in retirement. That means you’ll be moving to Akron Ohio, El Paso Texas or Grand Forks North Dakota where the cost of housing and food is low enough to make ends meet.

On a positive note, if you have any amount of money saved for your retirement, you’re ahead of half the households in the USA. If not, you can start saving now and leapfrog into the upper tier. But being ahead of a bunch of people who have no savings doesn’t mean you’re ready to retire. It doesn’t even mean you’re on track.

Before you despair, let’s see where you stand, and what you can do about it.

Average retirement savings

Average household savings by age is shown in the chart below. An average couple age 55 years old would have about $200,000 in savings.

$200,000 is a lot of money. Is it enough?

If you retired on that amount today, taking 4% out each year, you’d end up with about $667 a month. That, plus an average Social Security benefit of $1,543 gets you a retirement of $2,210 a month; more if both you and your spouse will receive Social Security benefits.

This could be a nice retirement for some, but you might want to target a higher figure for yours.

Your retirement savings — are you on track?

Most people say “as much as possible” when asked what their retirement savings should be. Others bark out “two million,” as if that’s some sort of magic number. The truth is that it’s different for each of us and that we all want to just keep living the way we always have.

Your retirement should be financially similar to when you were working.

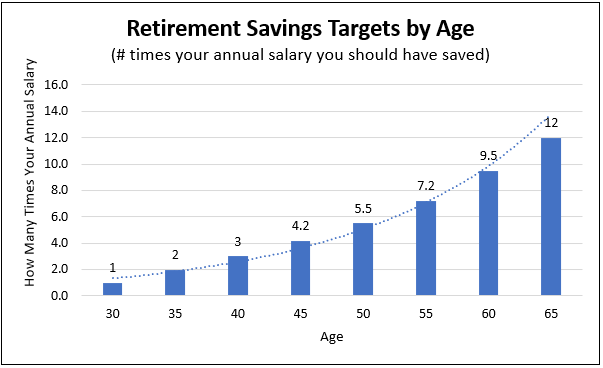

Most experts claim that you should have 8 to 12 years of salary saved up by the time you retire. That amount, coupled with your expected Social Security payments will provide you with a comfortable lifestyle.

It’s easy to calculate. Look at the chart below and multiple your salary times the number corresponding with your age. If you’re behind, you need to improve your position. If you’re ahead you can retire earlier or more lavishly.

If you’re 55 years old, earning $70,000 a year you should have $500,000 in your retirement accounts. Do you?

How to get more

Since half of all American households have no retirement savings to speak of, there’s a good chance you’re a bit behind your target. But don’t fret, there are plenty of options available.

1. Save and invest more

I realize this is the most obvious answer, but what’s not so obvious is how much to save.

The key to savings growth is the magic of compound growth. If you invest a little when you’re young, like the tortoise in the old fable, a small amount just keeps growing and growing. It’s different if you’re closer to retirement though. You’ll need to be more like the hare and invest quickly with larger amounts.

Use the chart above to get an idea of how much you’ll need. If you want to increase your retirement income by about $500 a month and have 20 years until retirement, you’ll want to invest about $300 a month. If you only have 10 years, you’ll need to set aside almost $1,000 a month.

2. Work longer

Working longer gives you two important financial benefits:

First, you’ll have more years to invest and more years for those investments to grow.

Second (it’s hard to consider this a benefit but it is), you’ll have fewer years to live so you can draw down your investments faster.

3. Downsize

With less money, you’ll have to find some ways to cut back on living expenses. Your single biggest category of costs will be related to housing (mortgage, taxes, utilities, upkeep). A smaller and less expensive home will help.

4. Spend less

Recognize the difference between “need” and “want”. I want to live in the style to which I’m accustomed. I need food to eat and shelter to keep the rain off my head. Focus on your needs when making purchase decisions.

5. Work part-time

You can supplement low savings with extra income. About 40 percent of retirees in their 60’s are enjoying a part-time encore career, and there’s no reason you can’t join them. Jobs are abundant right now and pay quite well. A post-retirement career provides purpose, engagement and eases the flow of limited funds.

When all else fails

You could scrimp and save throughout your retirement in a low-cost state like North Dakota, Texas or Ohio. Or you could consider living large in another country. There are plenty of tropical paradises with costs of living so low you can live like a king on a Social Security budget.

No matter what you do, the future is in your hands. You have the tools and ideas you need to make it the best it can be. All you need is dedication and passion, and that comes from the heart.

Make your retirement an awesome one! I know you will.